Peer payments on Messenger with PayPal and Venmo

Peer payments aims to develop consumer trust in payments on Meta and broad engagement with financial features in the United States, through building flexible payments with top payment providers.

My role

Staff Product Designer

Time

January 2024 – Present

My focus

Lead the design and partnership with market leaders in the US leveraging a hybrid approach, to drive growth for our consumer payments product in the US.

Team

2 product managers

8 engineering

12 XFN legal, marketing, compliance etc

20+ PayPal partners across functions

Context

Peer payments for Messenger in the United States struggled to grow to more than <1% of total marketshare, which is predominantly consumed by players such as Venmo, PayPal, Cash App and Zelle.

Strategically the team needed to re-evaluate viability of the company’s investment in peer payments. This led to our partnership with market leaders PayPal and Venmo, to build additional payment support on top of Messenger’s legacy card on file peer to peer product.

Problem

Historically, P2P on Meta Pay via debit cards has struggled to drive traction on Messenger. Meta owns the largest user network in the US; however, struggled to scale our native in-chat Meta Pay payment solutions due to:

-

Highly competitive market with deep pocketed players such as Zelle, Venmo, Cash App, PayPal and Apple Cash.

-

High competition, combined with slow progress on scaling hindered our ability to drive meaningful impact. Resources were pulled back, and years of underinvestment resulted in a suboptimal user experience.

-

Users were hesitant to store P2P credentials. Even those who completed onboarding feared scams, account hacking, and theft. This lack of trust resulted in no clear incentive for users to switch to Meta Pay P2P given established competitor P2P networks.

Send PUX

Receive PUX

Unilateral

US P2P was put into maintenance mode in August 2022, yet P2P is a valuable service as evidenced by the 7M+ users who send more than $9B annually. Since late 2022:

📉 Overall usage is declining

Since reducing features and putting the product on maintenance, we’ve had seen a 18% decline in MAU, 5% decline in L28 TPV

💵 Growing cost for low value

99% of the senders have a monthly transaction amount below $4,000 and 95% are below $1,600.

Despite, more than $100M in processing fees, plus operational overhead, and regulatory and servicing requirements

Strategic shift to hybrid payments

In the 2024, following the introduction of the success of the Hybrid Payments model I led in South East Asia & Brazil, across the organization we decided to pivot towards 3P platforms as this model addressed many of our previous scaling 1st party payment challenges:

-

Eliminates the need for users to create new payment accounts.

-

Leverages familiar 3P payment flows. Removes the need for users to store sensitive payment credentials.

-

Hybrid payments cost less to build since they don’t rely on heavyweight payments infrastructure, which in turn reduces regulatory and risk management overhead.

Hypothesis

By integrating with trusted payment services in America we are building more flexible, familiar, and trusted experiences that create higher app engagement for consumers and establishes FoA as a preferred channel for transactions and driving incremental business demand. In parallel, maintaining debit P2P, continues to provide proven value to our Ads ecosystem.

Project goals

Revitalize peer payments as an engaging, seamless, and habituating feature, by leading partnership with payment partners to increase payment optionality, ultimately offsetting and sunsetting the native debit card experience, driving efficiency, cost-saving, and greater user retention.

Metrics

Preserve P2P and $9B in annual TPV+ grow transaction volume

Offset over 250k annual open and processing with debit

Increase consumer engagement with payment features

Partner annual ad spend via contract (over 60M)

Finding a pilot partner

With the core team, I met with partnerships teams across CashApp, Zelle, and PayPal, to assess interest and investment into peer payments on Messenger and WhatsApp. PayPal (owner of Venmo) netted out to be the first partner for our new experience.

Over the course of 3 weeks, we met with a PayPal team of roughly 10 people, to share our existing product and vision for how integrations could quickly and seamless integrate into the chat experience.

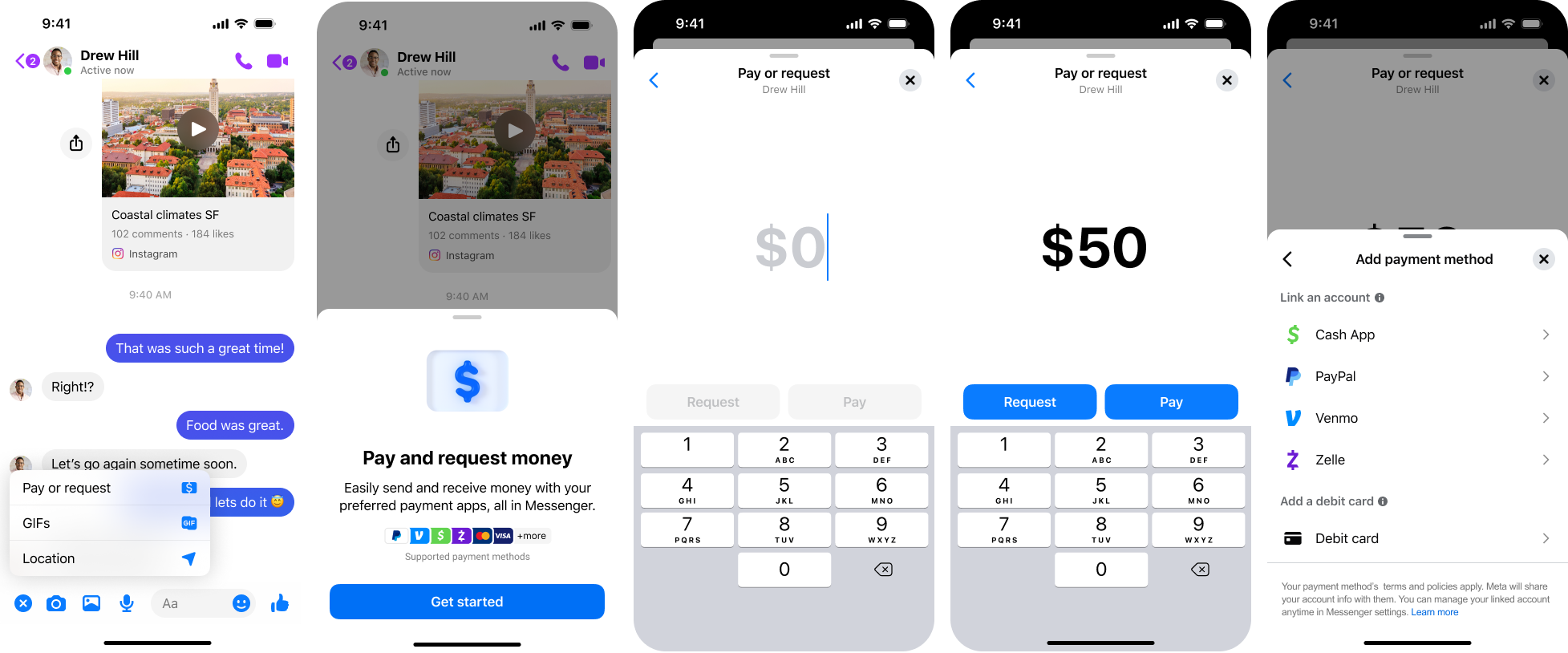

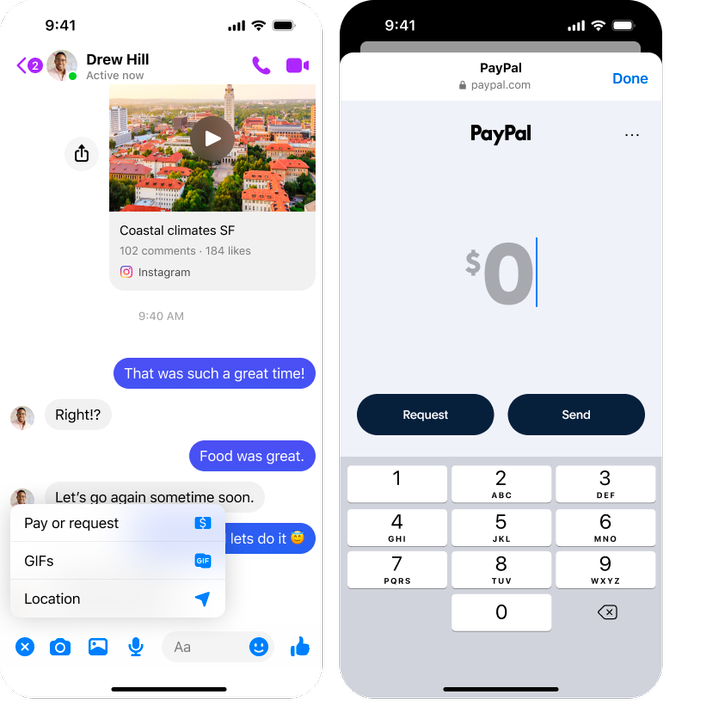

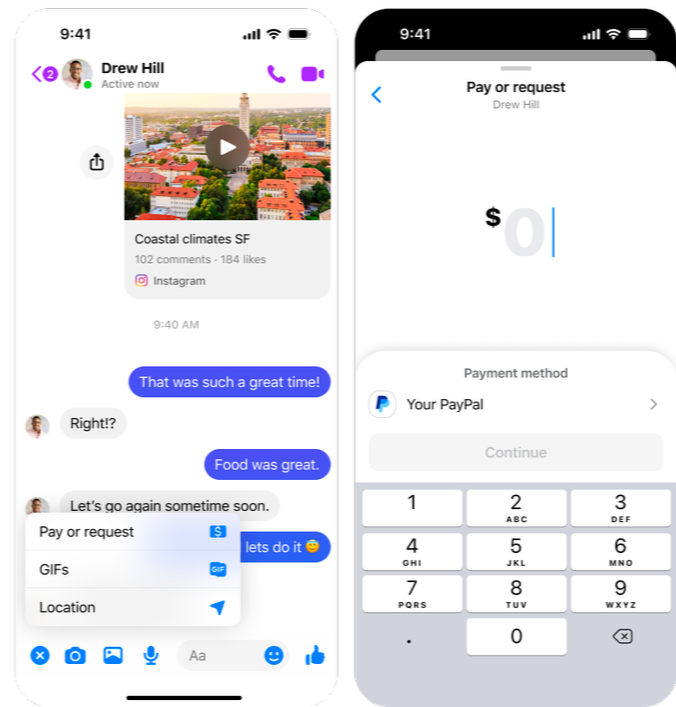

Chat integration hybrid UX discussion

Our main discussion point was the speed and level of integration for our pilot experience. Ultimately deciding on an integrated in-app-browser UX.

Option 1: In-App-Browser with Login

🟡 Medium speed to dev (.5-1 year)

🟡 Medium UX improvement

Option 2: Hybrid, app switch to PayPal w/ data passing

🟢 Fast speed to dev (.5 years)

🔴 Low UX improvement

Option 3: Linked account to Meta, embedded into native UI

🔴 Slow speed to dev (1-2 years)

🟢 High UX improvement

Through our discussions, we gained support and agreement for a o-auth powered, semi-native hybrid solution – Option 1.

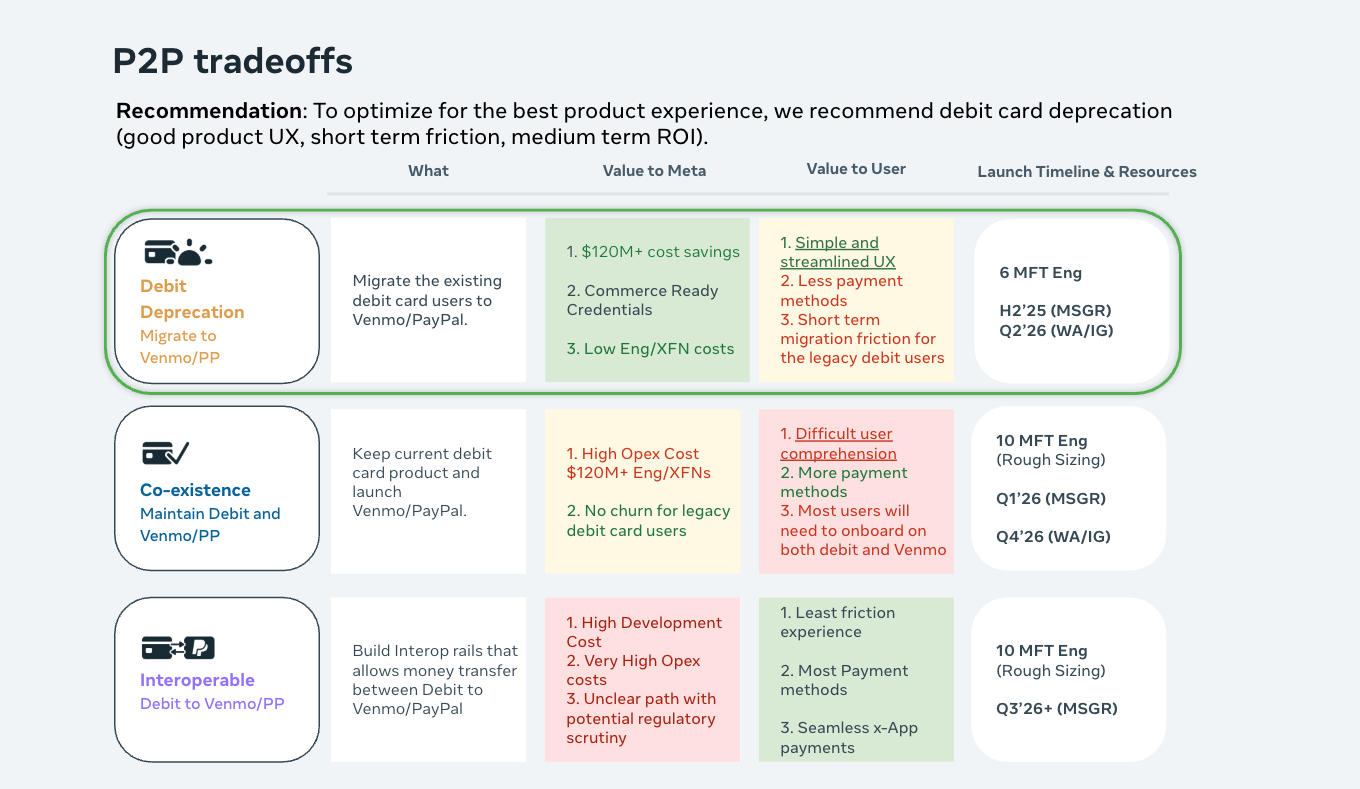

By doing so, we would sunset native debit card products, solely focusing on scaling payment facilitation via 3rd party partners, offloading overhead, costs, and difficult regulatory scrutiny.

Rapid prototyping

Constraints

Although PayPal and Venmo are now interoperable with one another, debit cards on Meta Pay would not be interoperable with those payment options. We are unable to invest in creating a new payment rail between our platform and PayPal, meaning user may only send between:

PayPal-Venmo to PayPal-Venmo

Debit to debit

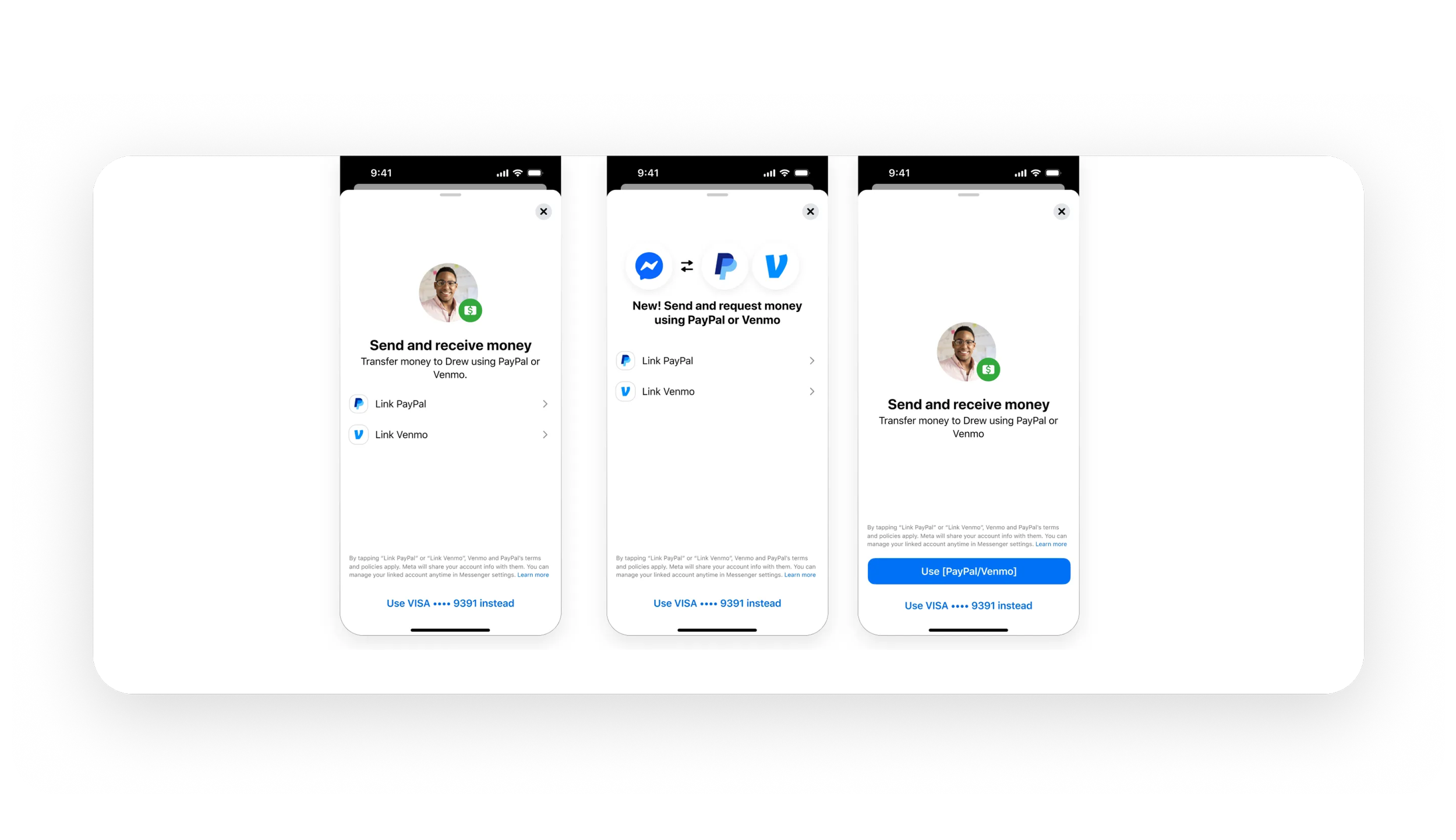

Onboarding - PayPal - One-Time-Password

Onboarding - PayPal - App authentication

PUX - PayPal - Send

PUX - Venmo - Receive

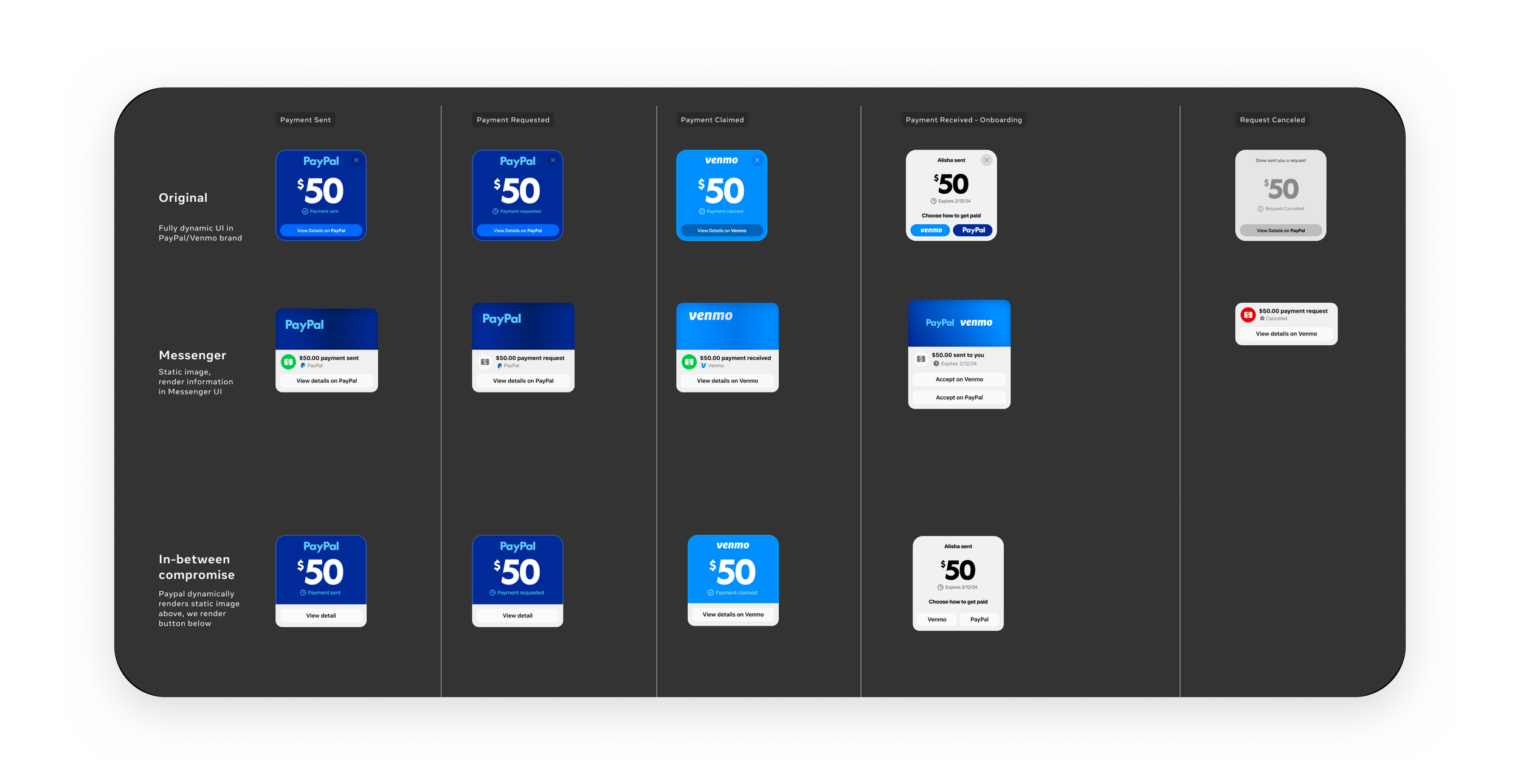

Payment bubble design

Evolving the payment framework established in South East Asia for Messaging Commerce, and as a part of PayPal’s new strategy for payments in many 3rd party chat apps and checkout experiences, the brand positioning and entry points were a vital consideration from both parties. Messenger’s strict design system and infrastructure requiring I lead months of iterations, alignments, and XFN discussion with leadership, design system teams, and branding both internally and externally.

Final alignment across 50+ states and statuses

Example of statuses and component in chat (Roughly 50 statuses)

After months of external and internal iterations and alignment, I drove align across MFT, Messenger, PayPal, and Venmo teams across 15+ stakeholders in design and product

Shift in leadership and strategy

Example of UX recommendation and product deck, provided to leadership

Context

In July 2025, Meta leadership changed, opening the discussion to reverse our decision to sunset the debit card features. After many rounds of reviews, the decision was made to retain debit for future possibilities and maintaining the payment licensing.

Impact/result

This resulted numerous follow-up reviews and discussion between the two companies, which I led during the absence of our PM. Ultimately gaining support from both Meta leadership and PayPal/Venmo to continue forward.

Keeping debit and managing difficult partner conversations

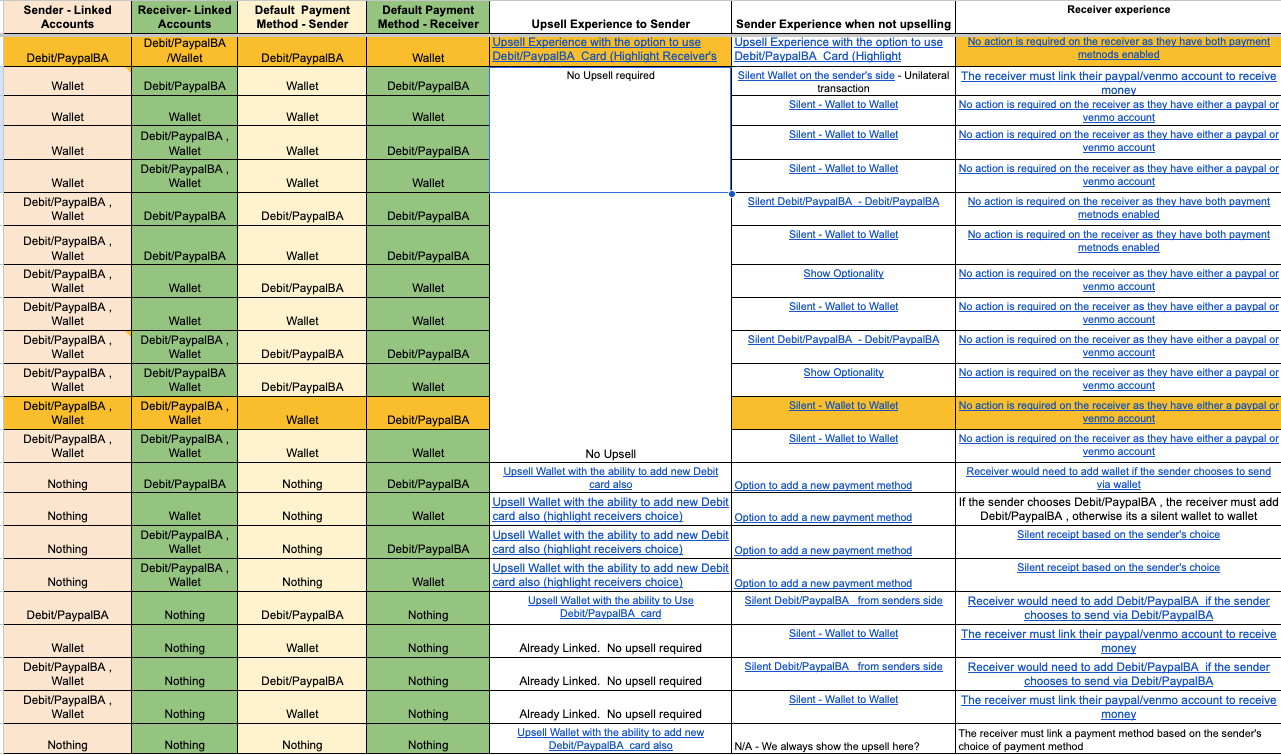

Due to the shift in strategy at the leadership level, we pivoted and made changes over the course of 1-month in continuous negotiation with PayPal regarding how we will now support PayPal/Venmo alongside an existing debit card product.

Requiring designs for over 120+ combinations of onboarding and error handling across Sender/Receiver experiences.

Driving clarity across companies for over 50+ scenarios

Example states for strategic upsells to new or existing p2p users

Example: Laying out the various combinations of user preferences and onboarding states with custom scenarios

With strategic shift, strong resistance from PayPal required significant new case-by-case handling to ensure existing users were given the chance to gain awareness of the new feature.

Due to the scale of possibilities of existing, new, or mixed credentials across both sender and receiver networks, I worked closely with engineering, product, and PayPal to negotiate the difficult conversations on onboarding/upselling new users.

Product launch

The product launched to 1% on March 30th and is currently at 50% roll out. Full general availability is slated for early May, 2026.

Our expected goal is to drive 500k L28 transactions by end of H1 2026 and 6.7M transactions across PayPal/Venmo integration.

Onboarding, NUX overview

Onboarding - PayPal - App Auth

Onboarding - Receiving a Payment

Returning user PayPal send

Future considerations / Looking ahead

I led our roadmap and strategic next vision for growth in consumer peer payments in 2026, across the Meta ecosystem. Our focus is on driving high-value, engagement opportunities to drive habituation and engagement with payment features on Meta’s apps.

Group splits

Expressive payments - Send

WhatsApp P2P

Partnering with product, I’ve envisioned our next steps for growth focused on driving total payment volume:

Group splits

+4-8% lift in total payment volume

Expressive payments

+2-3% lift in total payment volume

Web

+1-2% lift in total payment volume

WhatsApp

+30% lift in TPV